Legal recognition & rights

Legal recognition & rights Ready to register GST for Sole Proprietors and Freelancers

Get your GST registered at myHQ's provided premium addresses

Why should you get GST registration in India?

Legal recognition & rights Input tax credit Business expansion Need a government compliant office address for GST? Get a Virtual Office starting at ₹799/month

myHQ Assured

Pre-requisite for GST registration of Sole Proprietors and Freelancers in India

Trusted by

Everything you need to have in place before GST registration in India.

Step 1

Confirm your business address for GST

Provide a valid business address for your Sole Proprietors and Freelancers. Don’t have one? Use a government-compliant Virtual Office address to complete your GST registration seamlessly

GST Registration for Sole Proprietors and Freelancers: A Complete Step-by-Step Guide (2026)

Operating as a sole proprietor or freelancer in India means your business and your identity are legally one. There is no separate corporate entity. This makes GST registration a particularly direct process, but it also means errors in documentation can result in delays or rejections that affect your ability to invoice clients, claim input tax credits, and operate across state lines.

This guide covers every stage of the GST registration process for sole proprietors and freelancers in India, from eligibility assessment through post-registration compliance, as per the latest CBIC rules and guidelines applicable in 2026.

Table of contents

Table of contents

What is a Sole Proprietorship?

A sole proprietorship is the simplest and most common form of business structure in India. It is an unregistered business entity owned, managed, and operated by a single individual.

Unlike a Private Limited Company or an LLP, a sole proprietorship has no separate legal identity from its owner. The proprietor and the business are legally one and the same, meaning all income, liabilities, debts, and obligations of the business are personally attributed to the individual. There is no statutory registration requirement to form a sole proprietorship under any central legislation, though the proprietor may obtain registrations such as Udyam (MSME), Shop and Establishment licence, or Professional Tax registration depending on the state and nature of business.

For freelancers and independent professionals, the sole proprietorship structure is the default operating form unless a formal entity such as an LLP or Private Limited Company is incorporated. GST registration, where applicable, is obtained in the individual proprietor's PAN and Aadhaar, making the proprietor directly and personally responsible for all GST compliance obligations.

What is GST and why does it apply to sole proprietors

The Goods and Services Tax (GST) is an indirect tax levied on the supply of goods and services across India. Introduced on 1 July 2017, it replaced a fragmented system of indirect taxes including VAT, service tax, and excise duty under a single unified framework governed by the GST Council.

For sole proprietors and freelancers, GST is not a business-level obligation but a personal one. Since there is no legal distinction between the individual and the business under this structure, the proprietor is directly responsible for registration, return filing, and tax remittance. This applies whether you are a graphic designer, IT consultant, content writer, digital marketer, chartered accountant, or any other independent professional.

Who must register for GST

Registration under GST is mandatory when any of the following conditions apply.

Annual Turnover Threshold

| Category | Mandatory Registration Threshold |

|---|---|

| Service providers (most freelancers) | Annual aggregate turnover exceeds Rs. 20 lakh |

| Goods suppliers | Annual aggregate turnover exceeds Rs. 40 lakh |

| Special category states (Manipur, Mizoram, Nagaland, Tripura) | Annual turnover exceeds Rs. 10 lakh |

| Other North-Eastern and hill states | Thresholds as notified by respective state GST councils |

NOTE : Freelancers providing interstate services are not required to register under GST if their aggregate turnover remains below ₹20 lakh (₹10 lakh in special category states), as clarified by Notification No. 10/2017 under the IGST Act.

Under Section 23 CGST Act, GST registration is not required if a person:

- supplies only exempt services

- supplies non-taxable services

Mandatory Registration Irrespective of Turnover

The following situations require GST registration regardless of annual income:

- Providing services to clients located outside India where payment is received in convertible foreign currency (export of services)

- Supplying goods or services across state boundaries (inter-state supply)

- Selling through e-commerce platforms such as Amazon, Flipkart, or Meesho

- Receiving services from foreign platforms subject to Reverse Charge Mechanism (RCM), such as Upwork, Fiverr, or Freelancer.com

- Voluntary registration, where turnover is below the threshold but the proprietor wishes to claim input tax credit

Important: Aggregate turnover is calculated at the PAN level, not per client or per project. If you earn Rs. 12 lakh from freelancing and Rs. 9 lakh from rental income, your aggregate turnover is Rs. 21 lakh, which crosses the threshold and makes GST registration mandatory.

Documents required for GST registration

| Document | Purpose / Notes |

|---|---|

| PAN Card of the proprietor | Mandatory. The legal name must exactly match the PAN record. |

| Aadhaar Card of the proprietor | Required for Aadhaar-based OTP authentication (recommended for faster processing) |

| Passport-size photograph | Recent photograph of the proprietor |

| Proof of principal place of business | Owned: electricity bill, property tax receipt, or ownership document. Rented: lease or rent agreement plus lessor’s proof of ownership |

| Consent letter (if premises belong to a relative) | Accompanied by the relative’s ID proof and ownership document |

| Bank account details | Cancelled cheque or bank statement in the proprietor’s name. Must be submitted within 30 days of registration or before filing GSTR-1 |

| Mobile number and email ID | Linked to Aadhaar for OTP verification |

DSC (Digital Signature Certificate) is not required for sole proprietors. Authentication is completed via Aadhaar OTP (e-Sign) or Electronic Verification Code (EVC).

Step-by-step GST registration process for sole proprietors and freelancers

Registration is completed entirely online through the official GST portal at gst.gov.in. There is no physical office visit required under standard processing.

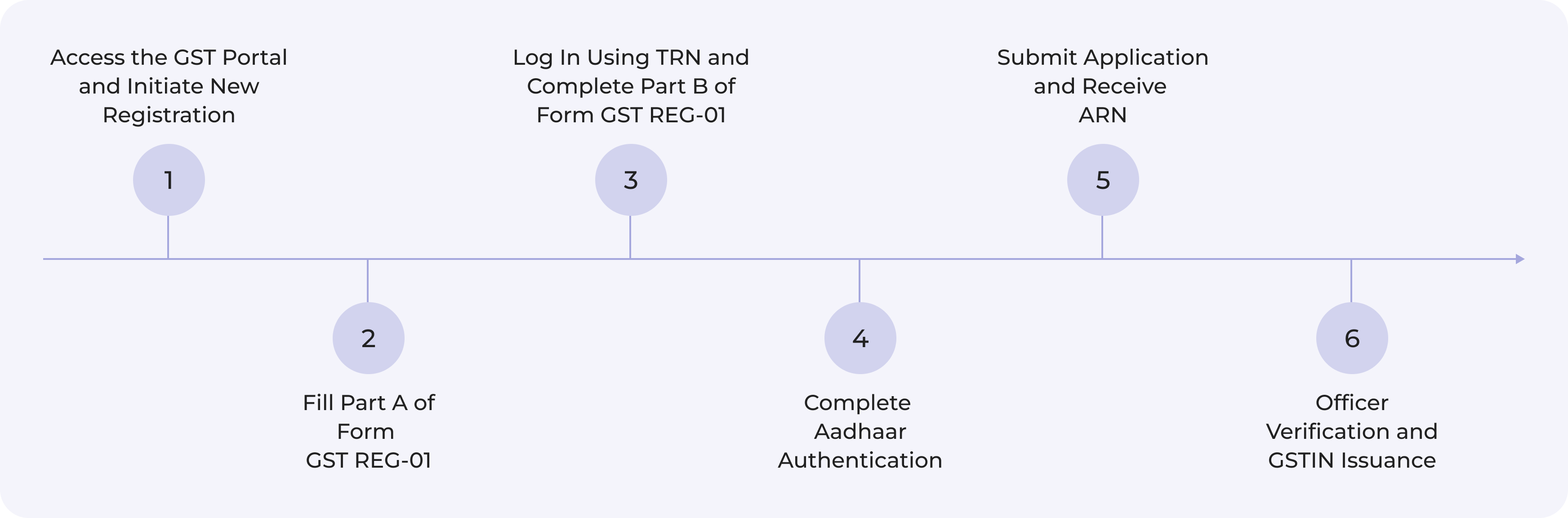

Step 1: Access the GST Portal and Initiate New Registration

Visit gst.gov.in. Navigate to Services > Registration > New Registration. Select "Taxpayer" from the taxpayer type dropdown.

Step 2: Fill Part A of Form GST REG-01

Enter your legal name as per PAN, PAN number, active mobile number, and email address. An OTP will be sent to both your mobile number and email ID. Verify both OTPs. Upon successful verification, a 15-digit Temporary Reference Number (TRN) is generated. This TRN is valid for 15 days only.

Step 3: Log In Using TRN and Complete Part B of Form GST REG-01

Log in to the portal using your TRN. Part B requires the following details: business constitution (Proprietorship), trade name if any, principal place of business address, HSN or SAC codes for your goods or services, bank account details, and upload of all required documents.

Step 4: Complete Aadhaar Authentication

Select Aadhaar authentication during the application. This is strongly recommended as it triggers the faster electronic registration pathway introduced under CBIC Rule 9A. An authentication link is sent to your Aadhaar-linked mobile number. Complete the OTP verification within the stipulated time.

Step 5: Submit Application and Receive ARN

Sole proprietors submit the application using Aadhaar OTP (e-Sign) or EVC. DSC is not required. Upon submission, an Application Reference Number (ARN) is generated and sent to your registered email and mobile number. Use this ARN to track your application status on the portal under Services > Registration > Track Application Status.

Step 6: Officer Verification and GSTIN Issuance

Your application undergoes automated and officer-level scrutiny. If documents are complete and Aadhaar authentication has been completed, GSTIN is issued within the prescribed timeline. The GST registration certificate (Form GST REG-06) is sent to your registered email address.

GST registration fees

| Fee Category | Amount |

|---|---|

| Government portal registration fee | Nil |

| GSTIN allotment fee | Nil |

| GST registration certificate fee | Nil |

| Professional or CA assistance (optional) | Rs. 500 to Rs. 1,500 for sole proprietors (market range) |

| DSC (not required for sole proprietors) | Not applicable |

GST registration through the official government portal at gst.gov.in is completely free of charge. The Government of India does not levy any fee for filing the application, verification, or GSTIN allotment.

GST registration processing timeline

| Application Type | Processing Timeline |

|---|---|

| Aadhaar-authenticated, low-risk application (Rule 9A / Rule 14A) | 3 working days (effective 1 November 2025) |

| Standard application with complete documents | 7 working days |

| Application flagged for physical verification (high-risk) | Up to 30 days. Physical verification must be completed at least 5 days before the deadline. |

| Clarification notice issued (Form GST REG-03) | Applicant has 7 working days to respond via Form GST REG-04 |

| Application with incomplete or mismatched documents | Delays vary. Rejection communicated via Form GST REG-05 |

As per CBIC clarification dated 1 June 2025, the average turnaround time across India is under 7 working days. Most delays are caused by incomplete documentation or OTP authentication failures, not systemic processing issues.

Applicable GST rate for freelancers and service providers

Most freelance and independent professional services in India attract GST at 18 percent under the standard rate applicable to services. This rate applies to services classified under SAC codes in the GST tariff schedule.

Exports of services, meaning services provided to clients outside India where payment is received in convertible foreign currency, are zero-rated. Registered freelancers exporting services may file a Letter of Undertaking (LUT) at the start of each financial year to invoice clients at 0 percent GST and later claim a refund of input tax credit through Form RFD-01.

Regular scheme vs composition scheme

| Factor | Regular Scheme | Composition Scheme |

|---|---|---|

| Eligibility by turnover | No upper limit | Up to Rs. 1.5 crore (goods); Rs. 50 lakh (services) |

| GST charged on invoices | Yes, at applicable rate (18% for most services) | No GST on invoices; pays fixed percentage of turnover |

| Input Tax Credit (ITC) | Claimable | Not available |

| Recommended for | Freelancers with corporate clients, export clients | Very small traders supplying only to end consumers |

| Return filing | GSTR-1 and GSTR-3B (monthly or quarterly) | CMP-08 quarterly; GSTR-4 annually |

Most freelancers and sole proprietors providing services to registered businesses should opt for the regular scheme. This allows clients to claim ITC on your invoices, which is often a prerequisite for enterprise and corporate engagements. The GST Composition Scheme is generally not applicable to freelancers or service providers except under the special composition scheme for service providers with turnover up to ₹50 lakh.

How Virtual Offices help with GST registration

One of the most common hurdles for sole proprietors and freelancers during GST registration is providing a valid, verifiable business address. A residential address may invite additional scrutiny during officer verification. myHQ Virtual Office provides GST-compliant registered addresses across 34+ cities in India, supported by 150+ partner spaces, 50+ Virtual Office Experts, and 10,000+ clients served.

- Digital KYC and agreement process, fully paperless

- Fastest document turnaround time in the industry

- Flexible contract tenures with no long-term lock-in

- Comprehensive help and support from 50+ Virtual Office experts

Whether you are a freelance designer in Bengaluru or a consultant operating from Jaipur, myHQ provides a credible business address that satisfies GST officer verification requirements. All lease documentation provided is specifically structured to meet GST registration requirements, reducing the risk of queries or rejection on address grounds.

Post-registration compliance for sole proprietors and freelancers

After receiving your GSTIN, the following compliance obligations apply.

GST Return Filing Schedule

| Return Form | Purpose | Due Date |

|---|---|---|

| GSTR-1 | Details of all outward supplies | 11th of the following month (monthly); 13th of the month following quarter (QRMP) |

| GSTR-3B | Summary of GST liability and ITC claimed | 20th of the following month (monthly); 22nd or 24th of the following month (QRMP, state-wise) |

| PMT-06 | Monthly tax payment challan under QRMP | 20th of each month |

| GSTR-9 | Annual return (mandatory above Rs. 2 crore turnover) | 31st December of the following financial year |

| GSTR-9C | Reconciliation statement (mandatory above Rs. 5 crore) | 31st December of the following financial year |

QRMP Scheme

If your aggregate turnover is up to Rs. 5 crore, you may opt for the Quarterly Return Monthly Payment (QRMP) scheme. Under QRMP, GSTR-1 and GSTR-3B are filed quarterly while tax is paid monthly via PMT-06. The scheme can be opted into or out of through the GST portal at the start of each quarter.

E-Invoicing Requirements

As of 1 August 2025, e-invoicing through the Invoice Registration Portal (IRP) is mandatory if your aggregate turnover has exceeded Rs. 5 crore in any financial year from 2017-18 onwards. Most freelancers and sole proprietors operating below this threshold are not required to generate e-invoices. However, this threshold must be monitored annually as your business grows.

Reverse Charge Mechanism (RCM)

Freelancers who receive services from foreign platforms such as Upwork, Fiverr, or Freelancer.com are treated as recipients of Online Information and Database Access or Retrieval (OIDAR) services. Under Section 5 of the IGST Act, 2017, the recipient in India is liable to pay GST under RCM. This amount must be calculated and remitted while filing your GST returns each period.

Invoicing requirements for registered sole proprietors and freelancers

Every tax invoice issued by a GST-registered sole proprietor must contain the following as per Rule 46 of the CGST Rules:

- Legal name as per PAN and GST registration

- GSTIN (15-digit GST Identification Number)

- A unique sequential invoice number (for example, INV-2026-001)

- Date of invoice

- Client name, address, and GSTIN if the client is a registered taxpayer

- SAC code for the service rendered

- Taxable value of the service

- Applicable GST rate and tax amount (CGST and SGST for intra-state; IGST for inter-state or export)

- Place of supply

Penalties for non-registration and non-compliance

| Non-Compliance | Penalty |

|---|---|

| Failure to register despite being liable | 10% of the tax due or Rs. 10,000, whichever is higher |

| Late filing of GST returns | Rs. 50 per day of delay (Rs. 20 per day for nil return filers), subject to a prescribed maximum cap |

| Not updating bank details within 30 days of GSTIN | Registration may be suspended, blocking GSTR-1 filing |

| Fraudulent registration or false information | Registration cancellation and penalties under GST law |

Common mistakes to avoid during GST registration

- Name mismatch between PAN, Aadhaar, and the registration form. Even minor discrepancies trigger rejection.

- Providing a residential address without adequate documentary proof. Rented premises require both the lease agreement and the lessor's ownership document.

- Failing to complete Aadhaar OTP authentication, which places the application in the slower processing queue.

- Not updating valid bank account details within 30 days of receiving GSTIN, which triggers registration suspension.

- Selecting incorrect HSN or SAC codes for the services rendered.

A word from our community.

myHQ has helped 10,000+ clients get their Virtual Office, boosting productivity and driving business growth.

myHQ Team provided great and fast support to us!

Great and fast service We needed an office for the registration of our company. We found Myhq through Google. The myHQ Team provided great and fast support to us. We recommend using the service of MyHQ once and you won't hesitate to use it again and again.

Harshit Arora

Director, Screen stitcheras

Get an address for your company

Stress free registrations guaranteed with myHQ

Get an address for your company

Stress free registrations guaranteed with myHQ

Frequently Asked Questions

Is GST registration mandatory for all freelancers in India?

GST registration becomes mandatory regardless of turnover when a freelancer sells through certain e-commerce operators required to collect TCS or is liable under Reverse Charge Mechanism. Interstate supply of services does not require registration if turnover is below ₹20 lakh (₹10 lakh in special category states), as clarified by Notification No. 10/2017-IGST.

Can a freelancer operating from home register for GST?

How long does GST registration take in 2026?

Does a sole proprietor need a DSC for GST registration?

What happens if I cross the turnover threshold mid-year?

Can I use a virtual office address for GST registration?